The Street's View

What Wall Street Is Saying

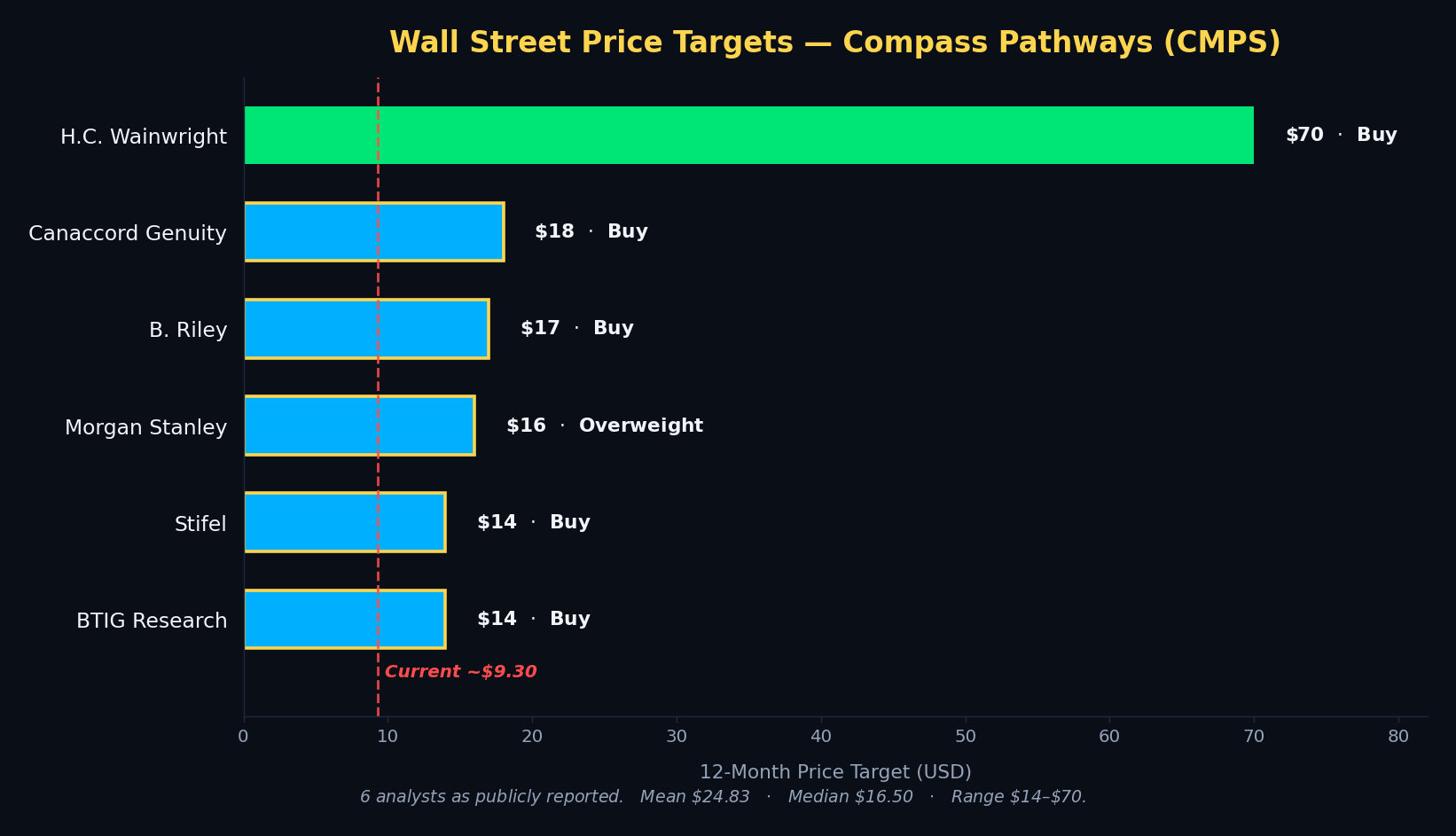

Wall Street is unusually unified on CMPS. Six sell-side firms publish active coverage, all with Buy or Overweight ratings. Targets range from $14 to $70, with a mean of $24.83 and a median of $16.50. From CMPS’s current ~$9.30, that implies roughly 77% upside on the median and 167% upside on the mean. The Street’s high target of $70 (H.C. Wainwright) implies more than a 7x from current levels — though we note H.C. Wainwright is a clear outlier; excluding it, the mean of the other five drops to $15.80.

Firm-by-firm analyst targets — H.C. Wainwright $70 Buy (raised from $40, Mar 2026), Canaccord Genuity $18 Buy, B. Riley $17 Buy (initiated coverage), Morgan Stanley $16 Overweight, Stifel $14 Buy (raised from $11), BTIG Research $14 Buy (reaffirmed Apr 20, 2026).